Inflation Headache

After January’s exciting finish amidst the GameStop saga, February felt like a return to some sort of normalcy. Investors turned away from the Reddit-fueled trading frenzy as they shifted towards common themes throughout the COVID-19 pandemic: economic recovery and vaccine distribution. February was a monumental month in the battle against COVID-19 with the FDA authorizing Johnson & Johnson’s single-shot vaccine for emergency use. The House of Representatives sent a $1.9 trillion COVID-19 relief bill to the Senate where it faces serious debate on several issues, including an increase in the minimum wage.

Despite the positive news, February’s equity rally fizzled out towards the end of the month. What shook the market? The answer lies with a rally in Treasury bond yields. The 10-year Treasury note started the year with a yield of roughly 0.90%. The late February rally pushed yields over 1.50%, the highest level since February 2020.

There are likely two causes of higher rates. Investors may be dumping their safety assets to take on more risk, signaling more confidence in equities moving forward. By selling their positions in treasuries, investors push down the price and cause yields to rise. Though this is certainly plausible, there is likely a bigger culprit at hand.

It appears the market caught a case of the inflation jitters. Inflation has been a heavily debated topic since the Federal Reserve first announced an inflation target in 2012. The Federal Reserve, along with other central banks, believes that a moderate inflation rate can promote a healthy economy. However, excessive inflation can be troublesome for financial assets and particularly devastating for fixed income securities. The interest received on a bond is typically a fixed rate. When inflation rises quickly, investors lose purchasing power on their interest income. Plus, prices of existing bonds drop to reflect higher rates available in the market.

Inflation has been a developing headache for investors since last summer. With improving numbers for the economy and more stimulus coming, inflation expectations have recently ballooned into a full-blown migraine. Investors fear that rising inflation could push the Fed to raise interest rates, a position Fed Chairman Jerome Powell has tried to assuage, pledging to maintain low rates while letting inflation run higher.

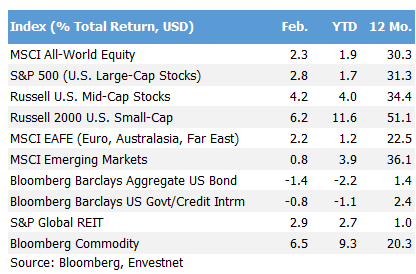

The rally in Treasury yields signals a better outlook for the economy, though not all asset classes, economic sectors, or factors respond the same way. Rising interest rates essentially cause investors to rethink how much they are willing to spend for a piece of the pie. Companies with relatively high price-to-earnings ratios, like Apple and Tesla, led the selloff as investors revalued growth stocks. However, value stocks, companies with relatively low price-to-earnings ratios, held their own amidst the selloff. The same contrast is evident in foreign markets, where emerging markets underperform as investors move their risk capital to more developed market assets. The financial sector, whose earnings are sensitive to changes in interest rates, stands to benefit from rising rates, while the real estate sector may cool off as higher rates deter potential buyers.

What it All Means

Inflation pressures are unsettling for investors. Though the Fed’s guidance has improved investor sentiment in the short term, many expect long-term inflation to continue rising throughout 2021. Every investor wishes they had a crystal ball - a way of predicting a very uncertain future. Unfortunately, trying to predict the future, particularly in financial markets, is often a loser’s game. Broad diversification and consistent exposure to financial markets has proven be the best hedge against short-term volatility. Inflation can eat at bond returns or change the way we value a company’s earnings. However, inflation is cash’s biggest enemy. An asset allocation based on a tailored, long-term financial plan will carry you through uncertain times.

Contact us at 865-584-1850 or info@proffittgoodson.com

Please see disclosures