Mercurial Market

Quick Take

November saw brief volatility driven by risk-off sentiment, AI-stock swings, shutdown-related data gaps, and shifting Fed cut expectations, but most asset classes stabilized by month-end.

Despite short-term pullbacks, 2025 has delivered strong YTD gains across stocks and bonds; the takeaway into year-end is to stay disciplined, diversified, and focused on long-term allocation rather than headlines.

November Market Recap and Year-End Perspective

November brought a brief bout of volatility across markets. Investors weighed concerns about AI-related stocks, the outlook for Fed rate cuts, and the impact of the government shutdown on economic data. By month-end, most asset classes stabilized, reinforcing an important message for long-term investors: short-term swings are normal, and disciplined portfolios are built to weather them.

Market Performance Snapshot

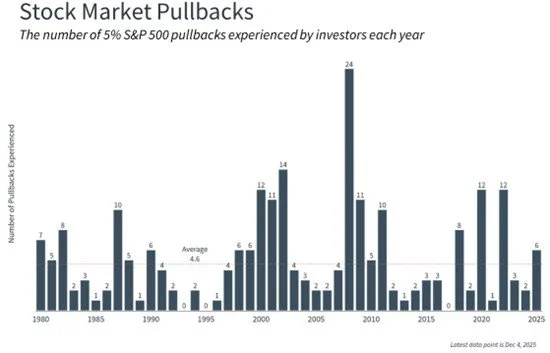

U.S. stocks: The S&P 500 settled up 0.1% in November after falling 5%, and is up 16% year-to-date. There have now been six declines of 5% or worse for the S&P 500 this year, the most since 2022 but close to the historical average.

International stocks: Developed markets rose modestly while emerging markets declined. Both have strong year-to-date returns, returning 24% and 27%, respectively.

Fixed income: Bonds advanced, with the Bloomberg U.S. Aggregate Bond Index up 1% in November and 8% YTD, helped by a decline in long-term yields. The 10-year Treasury ended near 4%.

Alternatives: Crypto saw a sharp pullback, underscoring its speculative nature. Bitcoin in particular has fallen over 30% from its early October highs. Gold finished higher but below October’s peak.

What Drove Markets in November

A temporary “risk-off” shift.

Investors stepped back from higher-risk areas such as technology stocks, high-yield credit bonds, and cryptocurrencies amid valuation and sustainability debates. Some of these areas rebounded late in the month as fundamentals reasserted themselves.

AI volatility, but resilient fundamentals.

AI-related stocks had their weakest stretch since spring, driven by concerns over spending, margins, and bubble risk. Still, earnings results from key companies such as Nvidia highlighted continued revenue and profit strength, supporting a late-month recovery in parts of the sector.

Shutdown-driven data uncertainty.

The longest government shutdown in history delayed critical economic reports. The September jobs report showed softer but still positive growth, and October data will be incomplete. Markets largely looked through the shutdown, but reduced visibility increased short-term uncertainty.

Shifting Fed expectations.

With fragmented data, rate-cut probabilities moved sharply during the month. Markets now expect a cut in December, with potential follow-ups in 2026 depending on growth and inflation trends.

Staying Grounded Into Year-End

Market pullbacks and reversals like November’s are a feature - not a flaw - of investing. The year has delivered strong gains across stocks and bonds, and short-term volatility doesn’t change the long-term case for maintaining diversified exposure aligned to your goals.

As we approach year-end, the key is to remain focused on your strategic allocation, risk management over headlines, and long-term planning over short-term positioning. We’ll continue monitoring markets and opportunities closely, and we’re here to discuss any portfolio or planning questions as we head into 2026.

Contact us at 865-584-1850 or info@proffittgoodson.com