Navigating Policy, Technology, and Geopolitical Risk

Quick Take

Policy, technology disruption, and geopolitical tensions drove market volatility in February, highlighting how non-economic factors can influence investor sentiment.

The sell-off in software stocks and geopolitical headlines reflect shifting expectations rather than structural damage to the global economy or corporate earnings.

For investors, periods of volatility create opportunities to rebalance portfolios and add to high-quality investments while maintaining diversified exposure to multiple risks.

If you tried to follow the markets in February, it may have felt like the ground kept shifting beneath your feet. One day the headlines were about tariffs, the next about artificial intelligence, and soon after about tensions in the Middle East.

Yet the underlying economy didn’t change very much at all.

Inflation continues to cool slowly, and investors are still debating when the Federal Reserve might return to cutting interest rates. Against that fairly steady backdrop, global equities turned in mixed results during the month while bond markets remained relatively calm.

What captured investors’ attention instead were three developments - one in Washington, one in Silicon Valley, and one in the Persian Gulf.

A Court Decision That Matters for Trade

The Supreme Court’s ruling challenging the administration’s use of the International Emergency Economic Powers Act (IEEPA) to impose sweeping tariffs removed a meaningful policy tail risk for global trade.

The Court determined that the statute did not authorize tariffs of the scope implemented by the administration, effectively eliminating a key legal pathway for broad, unilateral tariffs. While the ruling does not eliminate the possibility of future tariffs, it suggests that additional trade restrictions are more likely to proceed through established statutory mechanisms that require formal investigations and longer implementation timelines.

The decision reduces the risk of sudden and large-scale trade actions that could disrupt global supply chains. Future tariff policy is likely to be more targeted and predictable, conditions that financial markets generally absorb more smoothly than abrupt policy shifts.

AI, Software, and Broadening Market Leadership

Meanwhile, software stocks had a rough February as investors reassessed growth expectations across the sector. While elevated valuations and sensitivity to interest rates contributed to the decline, advances in generative AI intensified concerns that parts of the traditional Software-as-a-Service (SaaS) model could face structural disruption.

The release of new AI tools capable of performing complex enterprise workflows - such as coding, legal review, and data analysis - prompted a broader reevaluation of software valuations. Anthropic’s introduction of advanced “agentic” systems, including Claude Cowork, reinforced the view that AI platforms may increasingly automate tasks traditionally supported by enterprise software applications.

At the center of this debate is the seat-based pricing model used by much of enterprise software. Companies typically pay for software based on the number of employees who use it. If AI allows fewer workers - or even autonomous systems - to perform the same tasks, businesses may ultimately require fewer software licenses, raising questions about the long-term growth trajectory of SaaS providers.

Notably, the weakness was concentrated in software companies rather than the broader technology sector. Other areas of information technology - particularly semiconductors and AI infrastructure - held up well, highlighting a growing divergence within the sector. More broadly, returns are increasingly being driven by a wider range of economic sectors rather than the narrow group of mega-cap technology companies that dominated performance in recent years.

In this context, the February software correction reflects a reassessment of how value may ultimately be distributed across the technology stack. Capital continues to heavily flow toward AI infrastructure - chips, data centers, and cloud computing - while the traditional application layer is being reevaluated for winners and losers.

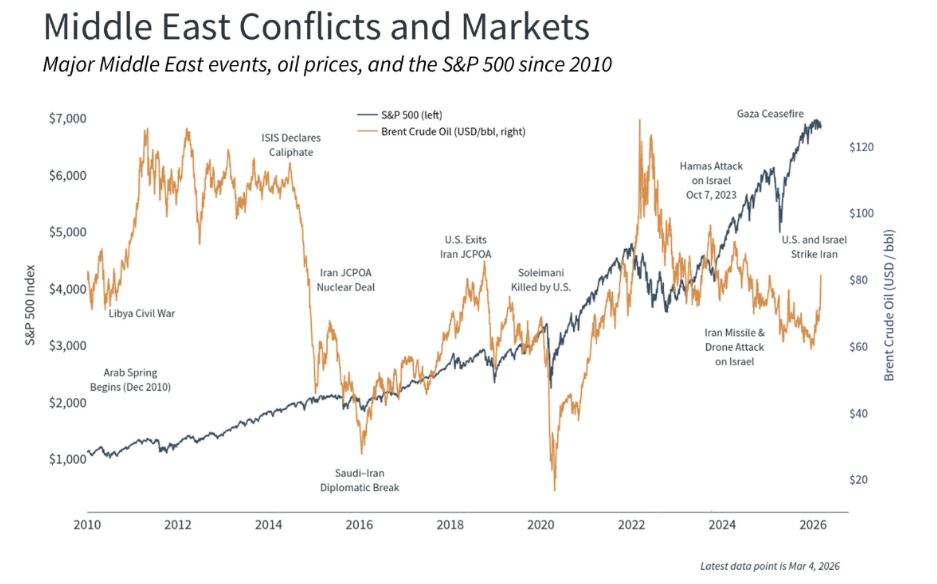

Geopolitics in the Middle East

Recent geopolitical developments in the Middle East have introduced modest volatility across global markets. Oil prices have moved higher as investors monitor potential risks to the Strait of Hormuz and Gulf infrastructure. Equity markets, however, have reacted in a measured fashion, with only modest declines and limited movement toward traditional safe havens, suggesting investors are assessing the situation cautiously.

History provides important context. Since World War II, major geopolitical events have typically produced short-term market declines averaging around 4%, with markets reaching a trough in a few weeks and recovering within about a month. While such moments can feel unusually dangerous in real time, financial markets - an aggregation of millions of views - often assess geopolitical risk as a recurring feature of the global landscape rather than a lasting threat to economic fundamentals.

For investors, the key question is whether the conflict materially disrupts global energy supply. If major shipping routes remain open and infrastructure remains intact, history suggests the broader economic and market impact is likely to be limited and temporary.

What This All Means

Taken together, February’s developments reflect a familiar pattern in financial markets. Policy decisions, technological shifts, and geopolitical tensions can generate sharp movements in individual sectors and create the appearance of heightened uncertainty. Yet for broadly diversified investors, such developments are rarely as consequential as they seem in the moment.

Trade policy rulings may influence the timing or structure of tariffs. Advances in artificial intelligence will reshape portions of the technology sector. Geopolitical tensions may periodically unsettle markets. History suggests, however, that markets tend to absorb these developments more quickly than investors expect.

Periods of uncertainty often create a powerful urge to act. Yet decisions made in haste - particularly during volatile moments - can carry lasting consequences. For long-term investors, the advantage lies less in predicting each policy shift, technological breakthrough, or geopolitical event than in maintaining a disciplined portfolio designed to navigate a wide range of possible outcomes.

The future will always bring developments that no investor can fully anticipate. Success in investing depends less on forecasting those events than on remaining patient, diversified, and focused on long-term objectives.

Contact us at 865-584-1850 or info@proffittgoodson.com