A Month That Defied Headlines

Quick Take

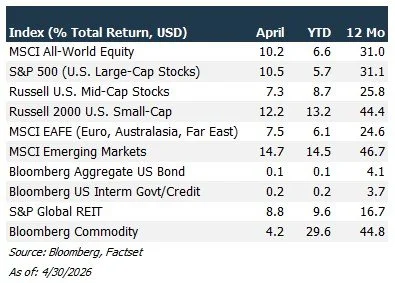

Global stocks posted one of their strongest months in years despite an active military conflict, surging oil prices, and deeply negative consumer sentiment — driven by corporate earnings that proved largely insulated from the geopolitical turbulence.

Enterprises are committing to AI infrastructure at scale, and the returns are arriving faster and at higher margins than Wall Street anticipated.

April is a case study in why market timing is so costly: the investors who stepped aside during March's selloff missed one of the best months for global equities in over five years.

Few investors would have predicted it entering April. Markets were navigating an active military conflict in the Middle East, oil prices near multi-year highs, and genuine uncertainty about the economic outlook. And yet, when the month was over, global stocks had posted one of their strongest performances in years. It is a reminder that when fear is priced into markets and fundamentals prove resilient, the recovery can be swift and powerful.

U.S. Stocks

The S&P 500 gained 11% in April, closing at a record high. The driver was corporate earnings, with artificial intelligence at the center: enterprises are committing to AI infrastructure at an accelerating pace, and the returns are arriving faster than Wall Street expected. Technology and communication services companies demonstrated that their businesses were largely insulated from the geopolitical turbulence playing out in energy markets, and because these companies represent such a large share of the overall market, their results had an outsized effect on index-level returns.

Artificial intelligence drove the headline results, but the earnings strength was broad-based. Industrials and real estate investment trusts (REITs) tied to data centers and financial companies performed well. Defensive areas — healthcare, utilities, and consumer staples — lagged as investors grew more confident and moved toward sectors with stronger growth potential.

US small-cap stocks surged roughly 12% in April, outpacing the S&P 500, as easing geopolitical tensions helped moderate inflation worries. Smaller U.S. companies offer attractive earnings growth at compelling valuations relative to large caps.

International Stocks

As geopolitical fears eased in April, the markets that had fallen furthest in March recovered with force. Developed international markets rose approximately 7%, while emerging markets surged 15%. South Korea and Taiwan led the way, benefiting from a powerful rebound in semiconductor companies such as TSMC, Samsung, and SK Hynix. A weaker U.S. dollar added further to returns for American investors holding international stocks.

April's international stock rebound was not an isolated event. International stocks have outperformed the S&P 500 dating back to January 2024, driven by attractive relative valuations, a weakening dollar, and accelerating earnings growth outside the United States — and that sustained outperformance has been a meaningful contributor to portfolio returns. The case for global diversification remains straightforward: international markets represent approximately 75% of global GDP, and the highest rates of economic expansion are projected to be outside U.S. borders. A globally diversified portfolio is built to capture it.

Bonds & The Federal Reserve

While equities captured the headlines, bonds were relatively muted. Interest rates ended April near where they began, with the 10-year Treasury yield finishing near 4.4%. Corporate bonds remained stable, with investment-grade spreads near their tightest levels historically — reflecting strong corporate fundamentals, though leaving limited room for further improvement. Bonds continue to offer meaningful income and stability — a contribution that is easy to overlook during strong equity months.

April also brought a leadership change at the Federal Reserve, with Kevin Warsh set to succeed Jerome Powell as Chair in May. Markets can be sensitive to transitions at the Fed — the Chair is its most powerful public voice — but interest rate decisions are made collectively by the twelve-member Federal Open Market Committee, and that institutional structure provides continuity. Warsh inherits a divided committee, and how he navigates that division while communicating the Fed's path forward on rates and inflation will be closely watched.

Why Staying Invested Matters

The tension at the heart of April — alarming headlines, exceptional returns — captures something fundamental about long-term investing. The instinct to step aside when uncertainty is high is entirely human. But acting on that instinct consistently leads to the same outcome: missing the recoveries that follow the fear.

Those who reduced risk in April missed the S&P 500's best month in over five years, a 15% surge in emerging markets, and a 12% rally in smaller U.S. companies. History consistently shows that the longer investors remain invested, the higher the probability of positive returns. Missing even a handful of the market's best days in any given decade can permanently reduce long-run wealth. And the investor who steps to the sidelines faces a second challenge just as difficult: deciding when it is finally safe to return. Diversification across geographies, company sizes, and asset classes is what allows a portfolio to capture recoveries wherever they occur — and April demonstrated that clearly.

Uncertainty is a permanent feature of markets, not a temporary one. The right preparation is a portfolio and a plan built to withstand it.

Contact us at 865-584-1850 or info@proffittgoodson.com