Higher Yields, Better Signals

Quick Take

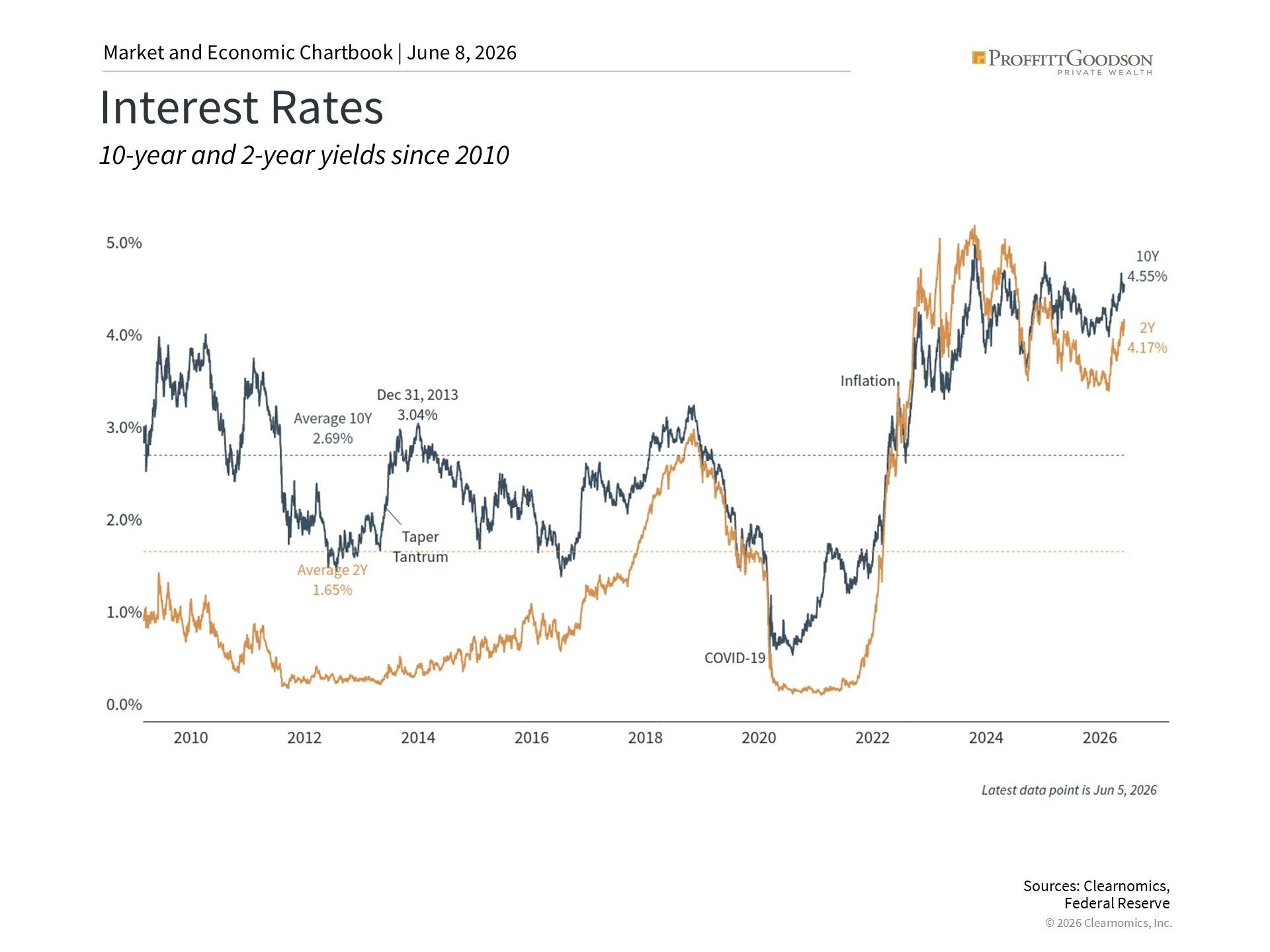

Interest rates were volatile recently as Treasury yields rose, driven by sticky inflation, shifting expectations for the Fed, resilient growth, and concerns about Treasury supply.

Higher yields can pressure borrowers, businesses, and asset prices in the short run, but they also make high-quality bonds more attractive by improving future return potential.

Rather than trying to predict the next move in rates, investors should recognize that today’s higher yields provide a better starting point for fixed income than in much of the post-financial-crisis era.

One of the more important recent market developments was the renewed volatility in interest rates. Long-term Treasury yields moved sharply higher during the month, with the 30-year U.S. Treasury yield briefly reaching its highest level in nearly two decades before settling back below 5%. The 10-year and 2-year yields rose as well, as investors increasingly concluded that interest rates may stay higher for longer than they had hoped.

The move was a reminder that, even after several years of rate volatility, the bond market can still surprise investors. Higher yields create discomfort in the short run, particularly for borrowers and for assets whose values depend heavily on future cash flows. But they also improve the long-term return potential of high-quality bonds.

Inflation Is Back in the Driver’s Seat

Bond markets rarely move for one clear reason. Recent inflation reports have come in hotter than expected, with energy prices playing a meaningful role. Higher gasoline and fuel costs matter not only because consumers notice them immediately, but because they can ripple through transportation, food, and goods prices if they persist.

Core inflation, which strips out food and energy, has also shown signs of stickiness. Some tariff-related price increases may be working their way through consumer goods, particularly in areas such as apparel. Meanwhile, strong demand for technology infrastructure, including AI-related chips and hardware, has contributed to price pressure in certain categories. These forces are less visible than gasoline prices, but they suggest that inflation pressures may not be confined to one temporary shock.

The Fed May Have Less Room to Move

Shifting views on the Fed have also impacted interest rates. Earlier this year, investors were still expecting the central bank to resume cutting rates. That expectation has faded. With inflation stubborn and the labor market still reasonably resilient, the Fed has had less reason to rush. Markets have adjusted to the possibility that policy may remain tight for longer, and perhaps even that the next move could be less friendly than investors had assumed.

Higher Rates Are Not Always Bad News

Higher yields are not necessarily a sign of trouble. Right now, growth is persistent, productivity is improving, and corporate activity remains healthy. Investors may demand higher real yields—the return above inflation—to part with their capital. That may be uncomfortable for borrowers, but it is not the same thing as a recession scare.

Treasury Supply Matters Too

Treasury supply and the Fed’s balance sheet are also part of the discussion. Investors continue to debate the sustainability of the current fiscal trajectory and how much support the Fed will provide as it reduces its own holdings of Treasuries. If investors believe they will be asked to absorb more long-term Treasury debt while the Fed is reducing its own holdings, they may demand higher yields.

The Bite of Higher Borrowing Costs

For consumers, higher interest rates affect mortgage rates, auto loans, credit cards, and other forms of borrowing. For businesses, they influence the cost of financing investment, expanding capacity, and making acquisitions. In markets, higher rates make future earnings worth a little less today, which can pressure stocks, real estate, and other assets whose value depends heavily on cash flows far into the future.

That is the part of the story investors tend to dislike. The other side deserves equal attention: higher yields also improve the prospective return from bonds.

The Better Starting Point for Bonds

The bond math is not complicated, but it is often forgotten when rates are moving quickly. The yield you earn when you buy a high-quality bond is not a perfect forecast of your future return, but over reasonable holding periods it has historically been a useful starting point. When yields are very low, future bond returns tend to be limited. When yields are higher, the math becomes more favorable.

Bond prices can still fall further if rates rise again. Investors were reminded of that in the post-COVID era. But the income cushion is now much larger than it was when yields were near zero, and that income can help offset some price volatility over time.

This is an important shift. For much of the post-financial-crisis period, bonds offered diversification but very little income. Investors owned them mostly for ballast. Today, bonds can once again contribute meaningful return potential to a diversified portfolio.

None of this makes rate volatility pleasant, but it does make it more tolerable.

Forecast Less, Plan Better

It is also worth keeping perspective. Interest rates have been unusually difficult to predict over the past several years. Markets have swung back and forth as investors revised their views on inflation, growth, geopolitics, fiscal policy, and the Fed. The same can happen again. A peace deal, softer inflation data, weaker growth, or a change in Fed communication could pull yields lower. A renewed inflation scare or stronger-than-expected economy could push them higher.

The point is not to forecast the next move in rates with false precision. The point is to recognize what today’s yields imply.

After years in which savers earned very little and bond investors had little margin for error, the starting point is now more attractive. Higher yields create challenges for borrowers and can pressure asset prices in the short run. But for long-term investors, they also restore something valuable: a reasonable expected return from high-quality fixed income.

Contact us at 865-584-1850 or info@proffittgoodson.com