A Mid-Year Review

Quick Take

The AI-driven rally kept the S&P 500's first half strong even as the "Magnificent Seven" lagged, with gains spreading to chipmakers, power providers, and infrastructure firms that had long stood outside the spotlight.

Rising yields dragged bond total returns down to roughly 1% for the half, but that same rise has repriced the asset class in investors' favor, improving future return potential.

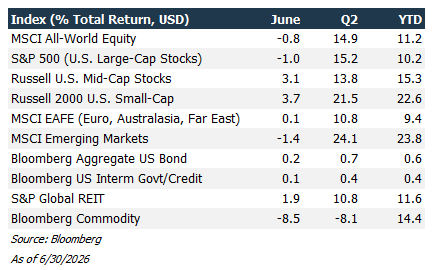

Few six-month stretches contain a war, a record-breaking rocket-maker's stock offering and a semiconductor boom all at once, but 2026 has managed it without breaking stride. The S&P 500 returned 10%, its best half-year since the pandemic snap-back of 2020. That the rally survived an oil shock, a new Fed chairman and the highest inflation reading in years says as much about investors' nerve as about the economy's, which is now seven years into an expansion many assumed would have ended by now.

The engine, as ever, is artificial intelligence. American tech giants are spending on data centers and chips at an unprecedented level, and profits have grown fast enough to keep the enthusiasm looking earned rather than merely hopeful. Memory companies, power providers, and other AI infrastructure have emerged as the biggest winners. Sandisk is up over 600% this year. SpaceX's blockbuster June listing, valuing it near $3trn at its peak, was less an outlier than a preview: OpenAI and Anthropic are expected to follow and broaden the opportunity set for investors.

The more interesting story than the headline index gain is what has been happening underneath it. The stocks that drove nearly every market gain of the past several years—the "Magnificent Seven"—have gone from carrying the index to lagging it, with six sitting in double-digit declines from all-time highs even as the broader market climbs, and volatility itself has stayed unusually calm throughout.

Meanwhile, a wider group of assets has quietly outrun U.S. large stocks: U.S. extended market stocks signal confidence in the economy, international shares are closing their valuation gap with Asian chipmakers adding AI exposure, and REITs have rallied despite rising rates, buoyed by cheap valuations and solid fundamentals. None of these was the obvious trade heading into 2026—a tidy rebuttal to the once-fashionable idea that concentrating in a handful of dominant firms was a free lunch.

Bonds had a more frustrating half-year. The ten-year Treasury yield climbed to nearly 4.5%, and the 30-year briefly touched its highest level in almost two decades. Since bond prices move inversely to yields, that climb ate into the income investors were collecting: the Bloomberg U.S. Aggregate index returned roughly 0.6% in total, despite bonds paying out considerably more along the way.

Several forces drove yields up. Kevin Warsh, sworn in as Fed chairman in May, has made clear that taming inflation still trumps supporting growth; traders have taken him at his word, pricing in further rate rises rather than the cuts many expected in January. Resilient growth has also lifted real yields, the return investors demand independent of inflation. And deficit concerns are pushing up longer-term yields, as investors charge more to hold debt issued to fund persistent borrowing.

Inflation itself flared up sharply. Brent crude spiked toward $120 a barrel in the spring, as the Iran war shut down shipping through the Strait of Hormuz, pushing headline inflation to its highest reading in years. Core inflation has proven stickier than oil alone would suggest: tariffs are pushing up the price of goods such as apparel, and demand for AI chips and hardware is adding pressure of its own—the same boom lifting stocks is, in its way, feeding the inflation the Fed is fighting.

Yet bond markets remain broadly sanguine that this is transient. Corporate bond spreads—the extra yield investors demand to hold corporate debt over Treasuries—have stayed historically tight throughout, a sign credit investors aren't pricing in distress. Oil has told a similar story, fully round-tripping back near pre-war levels, while Treasury and inflation-protected yields together imply investors expect inflation to settle just above 2% over the long run. That calm sits in tension with a Fed inclined to tighten—less a contradiction than a bet that Warsh's hawkishness is insurance against a shock, not evidence he expects one.

What It All Means

Strip away the noise and a single portfolio question emerges from both halves of this story. In equities, the AI trade has not ended so much as changed address: the fuel is reaching a much wider set of companies than it did a year ago—chipmakers, power providers, infrastructure firms—capturing gains once concentrated in a handful of household names, while other market segments post solid returns of their own. A portfolio still anchored to last cycle's winners is, in a real sense, underexposed to this one.

Bonds tell a quieter but arguably more useful story. Yield is not merely a bond's present-tense payout; it is, historically, one of the better predictors of what the asset will actually return over the years that follow. So while rising yields have weighed on prices this year, they have also repriced the asset class in investors' favor: anyone buying today is locking in income considerably richer than what was on offer for most of the past decade. Taken together with an equity market that is finally rewarding more than a handful of stocks, it makes a case for breadth, in both halves of the portfolio, that the last few years rarely did.

Contact us at 865-584-1850 or info@proffittgoodson.com